Discounted Gift Trusts: clever inheritance tax planning – or an expensive trap?

Inheritance tax planning in Britain increasingly feels like a race against time

House prices have soared, pension rules are tightening, and more middle-class families are discovering that a ‘wealthy estate’ now includes people who simply bought a decent house in the South East thirty years ago

Against that background, Discounted Gift Trusts (DGTs) have become a popular inheritance tax planning tool

Financial advisers often present them as offering the holy trinity of estate planning:

- immediate inheritance tax mitigation,

- retained withdrawals for life,

- and future investment growth outside the estate

And in fairness, DGTs can be highly effective.

But they aren’t magic.

Nor are they risk-free

Understanding both the advantages and disadvantages is essential before signing away large sums of capital.

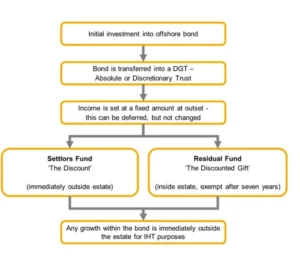

The attraction of DGTs

The basic appeal is straightforward

A donor places money – often into an investment bond inside a trust – while retaining the right to fixed withdrawals for life

Because the donor still benefits from those future withdrawals, HMRC accepts that not all the money has truly been given away

An actuarial calculation is therefore carried out.

This creates two elements:

| Element | IHT Treatment |

| Settlor’s Fund (the discount) | Immediately outside estate |

| Residual Fund | Outside estate after 7 years |

That distinction is the key

Unlike an ordinary gift – where the whole amount remains exposed for seven years – a DGT can create an immediate reduction in inheritance tax exposure from day one

For older retirees in particular, that can be extremely attractive

Immediate IHT mitigation

This is probably the biggest advantage

Suppose £600,000 is placed into a DGT, and the actuarial discount is calculated at £300,000

That £300,000 Settlor’s Fund immediately achieves inheritance tax mitigation.

Only the remaining £300,000 of the Residual Fund must survive for seven years

That means even if the donor dies relatively early, the planning may still produce meaningful inheritance tax savings

Compared with a standard outright gift, the ‘early death risk’ is softened considerably

Retained withdrawals

This is the other major attraction

Many retirees are reluctant to give away capital completely

A DGT offers a compromise.

The donor can continue receiving fixed withdrawals – perhaps 5% per year – while still reducing the eventual inheritance tax bill

Psychologically, that feels safer than simply handing large sums to children outright.

And for many people, it is

Future growth outside the estate

Another powerful feature is that future investment growth within the trust normally remains outside the estate

Over ten or fifteen years, this can become highly significant

Particularly where inheritance tax rates are effectively 40%, removing long-term growth from the estate can yield substantial savings for the next generation

But here come the problems

The issue with DGTs is that the tax advantages are easy to understand

The practical disadvantages are often less obvious

You no longer own the capital

This is the biggest downside of all

Once the money enters the trust:

- you usually can’t reclaim the underlying capital,

- even if your circumstances change dramatically later

You retain only the right to the predefined withdrawals.

That means the arrangement is fundamentally irreversible

If later in life you suddenly need:

- expensive care,

- medical treatment,

- family support,

- or higher income,

the trust capital itself is generally unavailable

That loss of flexibility can become uncomfortable – particularly as people move deeper into retirement

The withdrawals aren’t guaranteed forever

Many people mistakenly think of DGT withdrawals as ‘income’

In reality, they are usually withdrawals from an investment bond

If:

- investment returns are poor,

- markets perform badly,

- or withdrawals exceed growth,

the fund will gradually erode

And if the fund is exhausted, the withdrawals stop

This is not a guaranteed pension

It is still fundamentally an investment product

Inflation risk

A fixed withdrawal may feel generous initially

Ten or fifteen years later, it may not

Ten or fifteen years later, it may not

During periods of inflation, fixed withdrawals can lose real spending power surprisingly quickly

For retirees facing rising care costs, this can become a serious issue

Complexity and charges

DGTs aren’t simple arrangements

They involve:

- trust law,

- inheritance tax rules,

- actuarial calculations,

- investment bond taxation,

- and ongoing administration

They also frequently involve:

- adviser charges,

- wrapper charges,

- investment management fees,

- and sometimes exit penalties

Those costs can materially reduce long-term returns

The seven-year rule still matters

Although the Settlor’s Fund achieves immediate inheritance tax mitigation, the Residual Fund still depends on surviving seven years

So if death occurs early, part of the inheritance tax exposure may remain

A DGT reduces early-death risk. It doesn’t eliminate it.

The psychological reality

Perhaps the greatest issue is emotional rather than financial

A DGT works precisely because the donor genuinely parts with ownership of capital

Many people are comfortable with that initially

Years later, some aren’t

A common reaction is:

‘I didn’t realise how permanent this really was’

That is why DGTs are often most suitable for people who genuinely have surplus capital rather than simply ‘capital they hope not to need’

Discounted Gift Trusts can be highly effective inheritance tax planning tools

For the right person, they offer a rare combination of:

- immediate inheritance tax mitigation,

- retained withdrawals,

- and long-term estate reduction

But those benefits come at a price: loss of flexibility and permanent surrender of capital

And that is the real balancing act

The question is not simply whether a DGT saves inheritance tax

Often it will

The real question is whether the donor remains financially and psychologically comfortable with the arrangement for the rest of their life

Caveat emptor

Leave a reply

You must be logged in to post a comment.