The landlord squeeze: is Buy-to-Let still worth it after the Renters’ Rights Act?

For years, buy-to-let investors have complained that being a landlord in Britain has become a slow-motion game of regulatory whack-a-mole. First came the 3% stamp duty surcharge in 2016. Next, mortgage interest tax relief was curtailed under Section 24. EPC compliance costs rose. Licensing expanded. Capital gains tax allowances were slashed. And TODAY, May 1 2026, the biggest shake-up in decades arrives: the Renters’ Rights Act

For many accidental landlords and retirees who bought a flat ‘for income,’ this may be the final straw. But for professional investors? The story is more nuanced

How we got here: death by a thousand cuts

The golden age of buy-to-let was arguably 1996–2015. Cheap leverage, rising house prices, full mortgage interest relief and relatively light regulation created enormous wealth for landlords

Then the tide turned

The government increasingly viewed landlords as both politically expendable and partly responsible for housing affordability problems. Measures introduced over the past decade include:

- 3% stamp duty surcharge on second homes

- Reduction of mortgage interest tax relief for individual landlords

- Tougher affordability rules for buy-to-let mortgages

- Mandatory deposit protection schemes

- Licensing expansion for HMOs

- Stricter eviction procedures

- Proposed EPC upgrades

- Reduced CGT allowances on property disposals

Each measure alone was manageable. Together, they’ve squeezed smaller landlords particularly hard

A landlord with one mortgaged flat in London earning a 4% gross yield may now find that after mortgage costs, tax, maintenance, letting fees and void periods, the net return looks distinctly unimpressive

And now comes the biggest change yet

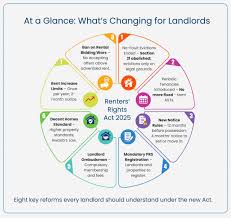

What changes on May 1?

From May 1, the Renters’ Rights Act fundamentally alters the balance of power between landlords and tenants in England

The biggest change is the abolition of Section 21 ‘no-fault’ evictions. Landlords will no longer be able to simply regain possession at the end of a tenancy without giving a reason. Instead, they must rely on Section 8 grounds such as rent arrears, anti-social behaviour, moving back into the property, or selling it

That matters because possession becomes slower, more administrative and potentially more litigious

Other major changes include:

- Assured shorthold tenancies disappear

- All tenancies become rolling periodic agreements

- Tenants can leave with two months’ notice

- Landlords will have to:

- provide tenants with information packs explaining how their rights have changed

- register themselves and their rental properties on a new Private Rented Sector Database

- register themselves with the new Private Landlord Ombudsman scheme

- Landlords can only raise rent once annually

- Tenants can challenge increases at tribunal

- Rental bidding wars are banned

- Landlords cannot refuse tenants simply because they have children or receive benefits

- Tenants gain stronger rights to request pets

Landlords wanting to sell or move back in must typically wait at least 12 months after the tenant moves in, then provide 4 months’ notice.

For good landlords, much of this may feel reasonable

For bad landlords, the era of easy evictions and minimal accountability is ending

Why many landlords are selling up

The UK has already seen an exodus of smaller landlords

Why?

Why?

Because many entered the buy-to-let market thinking it was passive income. It isn’t

It’s increasingly an operational business requiring:

- Legal knowledge

- Tax planning

- Maintenance oversight

- Tenant management

- Cash reserves

- Regulatory compliance

If your gross yield is 4% and your mortgage costs 5–6%, the maths can become brutal.

This is particularly painful in southern England, where yields are lower, and capital growth has slowed.

Why buy-to-let can still work

Here’s the contrarian view: buy-to-let is not dying – it’s professionalising.

Demand for rental property remains enormous. Britain still has a chronic housing shortage. Rental demand in cities such as Manchester, Birmingham and Leeds remains strong, and yields often outperform those in London

Professional landlords are adapting by:

- Buying in higher-yield regions

- Using limited company structures

- Focusing on HMOs or serviced accommodation

- Keeping lower leverage

- Treating property as a long-term business rather than a hobby

Ironically, as smaller landlords exit, reduced supply may push rents even higher – benefiting those who remain

So, is buy-to-let still worth it?

No, if:

- You’re highly leveraged

- You hate regulation

- You expect passive income

- You rely on easy capital growth

Yes, if:

- You buy at sensible yields

- You have strong cash reserves

- You understand tax structuring

- You’re willing to operate professionally

- You invest for 10–20 years, not quick gains

The old amateur landlord model is fading fast

Owning one heavily mortgaged flat and hoping tenants quietly pay your retirement income? That model looks increasingly fragile

But well-capitalised investors buying quality property in undersupplied rental markets may still do very well

Buy-to-let isn’t dead

It’s simply no longer easy

Leave a reply

You must be logged in to post a comment.