What is asset allocation – and how should it change as we age?

If you’ve ever wondered why some investors seem calmer during market swings, such as the one we’re experiencing now, the answer often comes down to one deceptively simple concept: asset allocation.

It’s not about picking the perfect stock. It’s about how you divide your money across different types of investments – and how that mix evolves over time

What is Asset Allocation?

At its core, asset allocation means spreading your investments across different “asset classes,” typically:

- Equities (shares) – higher growth potential, but more volatile

- Bonds (fixed income) – steadier, income-generating, but lower returns

- Cash – safe and liquid, but eroded by inflation

- Property or alternatives – can provide diversification and income

Think of it as your financial ‘balance of risk.’ The mix you choose determines how your portfolio behaves – how much it grows, how much it fluctuates, and how resilient it is in downturns

A younger investor might hold 80% in equities and 20% in bonds. Someone more cautious might reverse that

The key point? Asset allocation usually matters more than individual investment selection

Why asset allocation matters more than you think

Markets rise and fall unpredictably. But the structure of your portfolio determines how those movements affect you

A portfolio heavily weighted toward equities may grow faster – but it will also fall further in a downturn. A bond-heavy portfolio will probably be steadier – but may struggle to keep up with inflation

Good asset allocation aims to balance three things:

- Growth (to build wealth)

- Income (to support lifestyle)

- Stability (to help you sleep at night)

Get that balance right, and everything else becomes easier

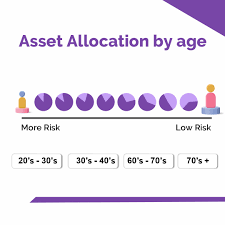

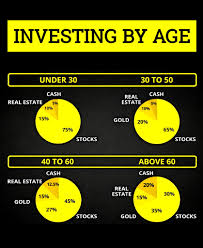

How asset allocation changes with age

This is where things get interesting – and personal

There’s a well-known rule of thumb:

Hold your age as a percentage in bonds

So at 70, you might have 70% in bonds and 30% in equities

But real life is more nuanced

NMTBP breaks it down by life stage

In your 40s and 50s: growth still matters

At this stage, you’re still building wealth and usually earning an income

Typical approach:

- Higher allocation to equities (60–80%)

- Some bonds for balance

- Limited cash holdings

Why? You have time to ride out market volatility. Short-term losses are uncomfortable – but not catastrophic

The biggest risk here is actually being too cautious and not growing your portfolio enough

In your 60s: the transition phase

Now you’re approaching retirement – or easing into it

Your priorities begin to shift:

- Protect what you’ve built

- Start thinking about income

- Reduce exposure to major market falls

Typical approach:

Typical approach:

- Equities reduced to around 40–60%

- Bonds increased for stability and income

- Some cash buffer introduced

This is often called the ‘de-risking’ phase

But here’s a crucial point: you haven’t finished investing. Your retirement could last 20–30 years. Growth still matters

In your 70s and beyond: income and stability

Now the focus is clearer:

- Reliable income

- Capital preservation

- Simplicity

Typical approach:

- Lower equity exposure (20–40%)

- Higher allocation to bonds and income-producing assets

- Cash buffer for 1–3 years of spending

This structure helps you avoid selling investments during market downturns – a key risk in retirement

The big mistake: becoming too conservative

Many investors become overly cautious as they age – moving too much into cash

It feels safe. But it can quietly erode your wealth

Why?

- Inflation reduces purchasing power

- Low returns limit growth

- You may outlive your money

Even in your 70s or 80s, some exposure to equities is usually essential

Think of it this way: your portfolio still needs to work for you – even in retirement

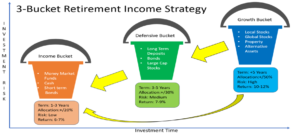

A more modern approach: the ‘bucket strategy’

Rather than thinking purely in percentages, many retirees now use a ‘bucket’ approach:

- Short-term bucket (0–3 years): cash and very low-risk assets

- Medium-term bucket (3–10 years): bonds and income funds

- Long-term bucket (10+ years): equities for growth

This can be psychologically powerful

When markets fall, you’re not forced to sell equities – you simply draw from your cash bucket

So what should you do?

There is no single perfect allocation. The right mix depends on:

- Your income needs

- Your health and life expectancy

- Your attitude to risk

- Other assets (property, pensions, etc.)

But a few guiding principles hold true:

- Stay diversified

- Adjust gradually, not dramatically

- Keep some growth assets at every age

- Review regularly (at least annually)

Final thought

Asset allocation isn’t a one-off decision – it’s a lifelong process

In your younger years, it’s about building wealth. In later life, it’s about preserving it – and making it last.

Get the balance right, and you give yourself something invaluable: financial resilience and peace of mind

Leave a reply

You must be logged in to post a comment.