Bond yields, debt interest, and the UK economy: why it all matters

Few financial indicators carry as much weight for the UK economy as government bond yields—the interest rates investors demand to lend to the state. Rising yields might sound like something that only City traders or economists worry about, but their effects ripple far beyond financial markets. They shape the government’s budget, influence mortgage costs, and ultimately affect every taxpayer

NMTBP explains

What are bond yields, and why do they move?

When the UK government borrows money, it issues gilts — bonds that pay a fixed interest rate (the coupon) and return the face value on maturity. The yield on a gilt is the effective rate of return investors earn based on its price

Yields rise when investors sell bonds, pushing prices down. They fall when investors buy bonds, pushing prices up. But behind these movements are deeper economic forces – especially expectations about inflation, Bank of England interest rates, and fiscal credibility

If inflation is high or markets fear that government borrowing is unsustainable, investors demand higher yields as compensation

Why rising yields increase the cost of debt

For a heavily indebted country like the UK, higher yields have an immediate fiscal consequence: they make borrowing more expensive

The government doesn’t pay off its entire debt every year – it rolls it over. As old gilts mature, new ones are issued to replace them. If those new gilts come with higher yields, the government must pay more interest

That means:

- Higher annual debt interest payments

- Less room for public spending or tax cuts

- Potentially higher deficits, as borrowing costs themselves rise

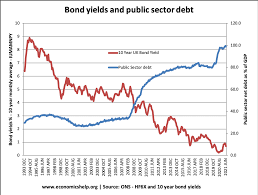

The UK’s public debt is now above 95% of GDP, compared to around 35% before the 2008 financial crisis. With that much debt, even a small rise in yields can add billions to the annual interest bill, which currently stands at £106 BILLION a year, more than the entire education and defence budgets!

The feedback loop: markets, policy, and confidence

Higher debt costs don’t happen in a vacuum – they feed back into market perceptions.

If investors start to worry about the UK’s fiscal sustainability, they may demand even higher yields, creating a self-reinforcing cycle of rising costs and weakening confidence

This was seen most dramatically in the autumn of 2022, when the Truss government’s mini-budget triggered a sharp spike in gilt yields. Investors lost faith in the UK’s fiscal credibility, sterling fell, and pension funds faced liquidity crises. The Bank of England had to step in to stabilise the market

The episode was a reminder that bond markets can discipline governments, especially those running large deficits in a world of higher interest rates

The wider economic impact

Rising gilt yields also affect the broader economy by setting a benchmark for other interest rates:

- Mortgage rates are influenced by gilt yields, particularly those on shorter-dated bonds

- Corporate borrowing costs rise, discouraging investment

- Consumer confidence can weaken as debt servicing costs rise and public finances tighten

In short, higher bond yields act as a drag on growth, even as they reflect market worries about inflation or fiscal policy in the first place

The policy dilemma

For the Treasury and the Bank of England, the current environment poses a dilemma

- The Bank’s focus on fighting inflation has meant keeping interest rates high

- The Treasury faces a mounting interest bill — projected by the Office for Budget Responsibility to exceed £100 billion in some years

That squeezes public finances and limits room for new spending commitments or tax cuts — especially ahead of elections. It also makes long-term investment harder, since short-term fiscal pressures dominate political decisions

That squeezes public finances and limits room for new spending commitments or tax cuts — especially ahead of elections. It also makes long-term investment harder, since short-term fiscal pressures dominate political decisions

The bigger picture: the end of cheap money

For much of the 2010s, the UK benefited from a world of ultra-low interest rates. Debt was cheap, and markets were forgiving. Those days are gone. The combination of persistent inflation, global rate rises, and geopolitical uncertainty has re-priced risk everywhere

For the UK, this means that fiscal discipline matters again. Markets are watching not only how much the government borrows, but whether it has a credible plan to manage debt sustainably. In that sense, bond yields are more than just a market statistic – they’re a barometer of economic confidence

In Summary

| Key Idea | Why It Matters |

| Rising bond yields | Signal higher borrowing costs for the UK government. |

| Higher debt interest | Consumes more of the public budget, reducing fiscal flexibility. |

| Market confidence | Determines whether yields rise due to fear or fall due to trust. |

| Wider economy | Feels the impact through mortgages, business loans, and consumer spending. |

Bond yields may seem abstract, but they sit at the heart of the UK’s economic story. They measure not just the price of money, but the price of credibility. As Britain navigates the challenges of high debt, ageing infrastructure, and slower growth, managing those yields – through sound policy, fiscal honesty, and stability – will be as crucial as any headline tax cut or spending plan

Leave a reply

You must be logged in to post a comment.